“Do more of what you love, less of what you tolerate and none of what you hate.”- Unknown🙏

A ‘Ross Mathematics Program’ child prodigy, a Forbes ‘30 under 30’ lawyer, a ‘NY food guide featured’ chef – these are my 3 young protagonists who embody this inspiring quote !

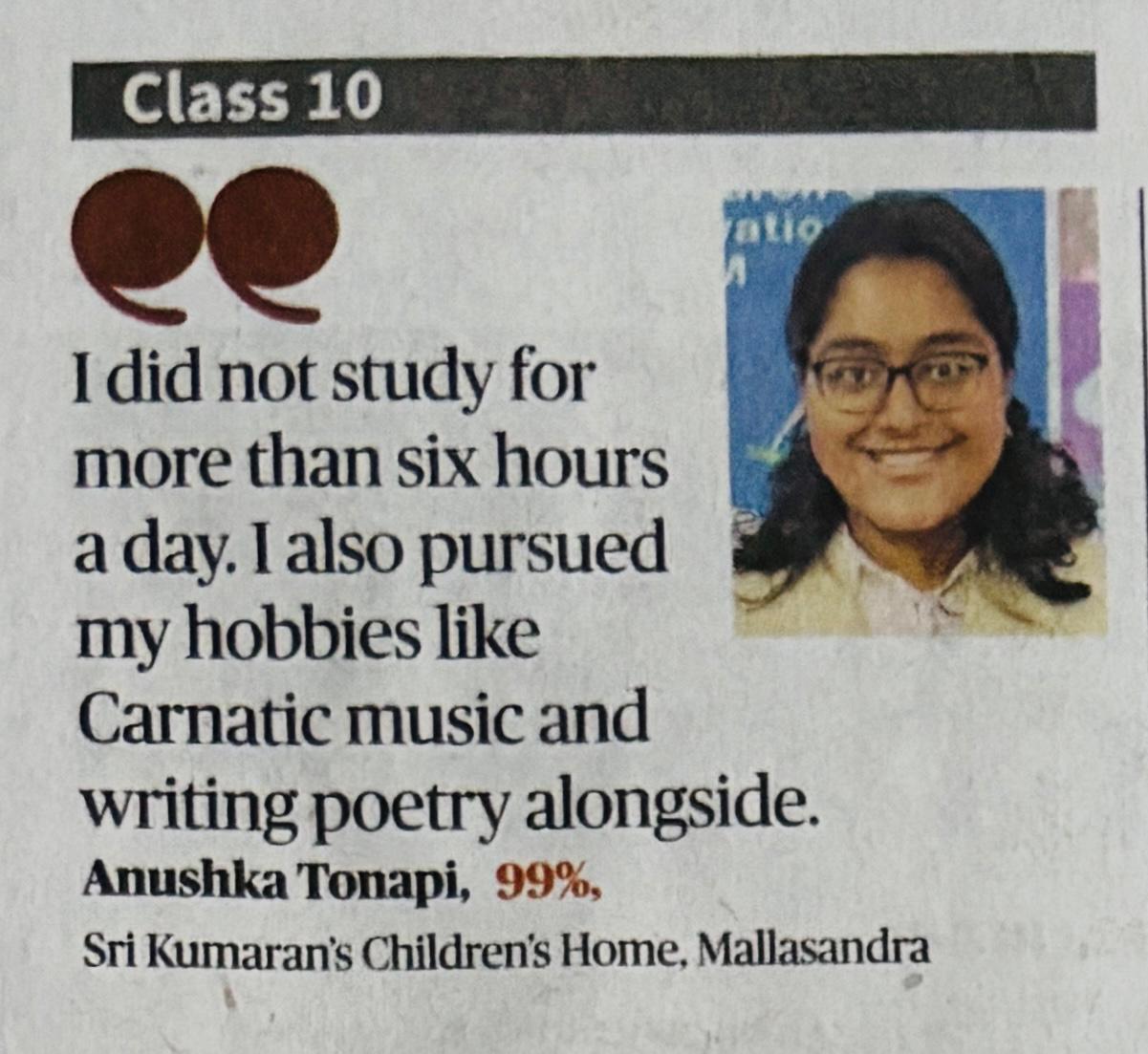

- First in line, the youngest of the lot. All of 15 years – Ms. Anushka Tonapi who has just graduated out of high school, scoring a whopping 99% in 10th grade alongside pursuing other interests close to her heart.

I have seen her as a little child contributing poetry to Children’s World magazine published by CBT children’s book trust, winning Commonwealth Essay Contest Gold and Silver awards and as a teenager, displaying her rich oratory skills on complex topics on a number of occasions. She is a young leader with a heart, a disability advocate creating awareness about Clubfoot which is a congenital foot disorder.

I have seen her as a little child contributing poetry to Children’s World magazine published by CBT children’s book trust, winning Commonwealth Essay Contest Gold and Silver awards and as a teenager, displaying her rich oratory skills on complex topics on a number of occasions. She is a young leader with a heart, a disability advocate creating awareness about Clubfoot which is a congenital foot disorder.

What Anushka loves most (as I understand) is NUMBERS. A child math prodigy who is currently interning at the Dept. of Mathematics, Indian Institute of Science (IISc) in ‘Linear Algebra’ (beyond my comprehension 😊), she has been accepted into the prestigious 6-week Ross Mathematics Programme (just 15% acceptance rate across the globe), in the Otterbein University in Columbus, Ohio, United States focused on advanced number theory and mathematical thinking for mathematically gifted students from around the world.

- Second one to feature is Ms. Vibha Nadig, a young and

dynamic lawyer from India’s premier National Law School. Apart from scholastic excellence, as a teenager she reached the highest levels at MUN (Model United Nations), an academic simulation where students engage in debates, research, and drafting resolutions to address global issues, mimicking the work of the United Nations that fosters valuable skills like public speaking, writing, and teamwork.

dynamic lawyer from India’s premier National Law School. Apart from scholastic excellence, as a teenager she reached the highest levels at MUN (Model United Nations), an academic simulation where students engage in debates, research, and drafting resolutions to address global issues, mimicking the work of the United Nations that fosters valuable skills like public speaking, writing, and teamwork.

Vibha loves working with PEOPLE and for people. Even as a student pursuing law, she felt the need to empower the marginalised with last mile justice delivery. Founder of what is today a unique not-for-profit company (https://www.outlawedindia.com/), she conceptualised and started the initiative back in her law school days creating awareness about legal rights, training the underprivileged to become para legals and serve their underserved communities. At 25, she has been recognised as one of the Forbes Asia LLC “30 UNDER 30” Class of 2025 in the Social Impact Category !

(https://www.forbes.com/30-under-30/2025/asia/social-impact).

- Last (but not the least) one in my ‘picklist’ is Chef

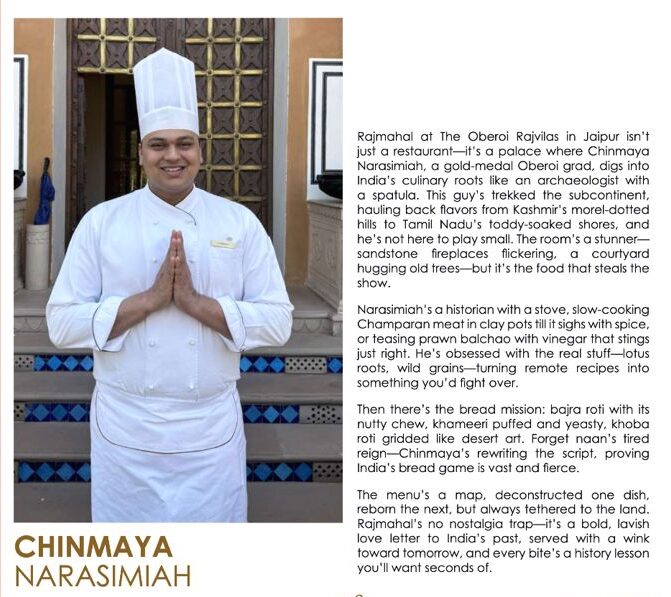

Chinmaya Narasimiah, a young, versatile chef at the Raj Vilas Oberoi, Jaipur specialising in Indian cuisine. Even as a young boy, his first love was FOOD – dreaming of food, enjoying as a foodie, conjuring up restaurant-like menus, sketching them, serving guests in style and most importantly checking out food in all events as an unofficial ‘taster’, evaluating if it is worth a try or not ! This soon turned into a passion and ultimately into his profession that looks glamourous but can be punishing at times. From being a co-author of a Coffee Table Book on ‘Karnataka Cuisines’ published by his Hotel Management college for the Ministry of Tourism to winning a gold medal at the Oberoi Centre for Learning & Development, his recent recognition has been, being featured in the New York Food Guide (https://thegastronomesguide.com/gastronomes-guide-2025/) along with several other seasoned chefs across India ! As a parent who saw and stood by him through his initial academic struggles, it is indeed a proud moment for me.

Chinmaya Narasimiah, a young, versatile chef at the Raj Vilas Oberoi, Jaipur specialising in Indian cuisine. Even as a young boy, his first love was FOOD – dreaming of food, enjoying as a foodie, conjuring up restaurant-like menus, sketching them, serving guests in style and most importantly checking out food in all events as an unofficial ‘taster’, evaluating if it is worth a try or not ! This soon turned into a passion and ultimately into his profession that looks glamourous but can be punishing at times. From being a co-author of a Coffee Table Book on ‘Karnataka Cuisines’ published by his Hotel Management college for the Ministry of Tourism to winning a gold medal at the Oberoi Centre for Learning & Development, his recent recognition has been, being featured in the New York Food Guide (https://thegastronomesguide.com/gastronomes-guide-2025/) along with several other seasoned chefs across India ! As a parent who saw and stood by him through his initial academic struggles, it is indeed a proud moment for me.

What is the secret sauce of their achievements ? Apart from their LOVE for their calling, as someone said “Stop doing things for joy, start doing them out of joy”.

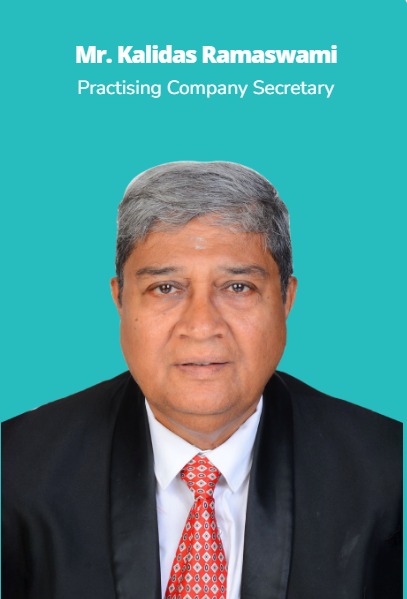

Let’s move on to the other sections of this 312th issue of Samhita. In our previous issue of Samhita, we had summarized about the clarification issued by SEBI on the position of Compliance Officer under Regulation 6 of SEBI LODR. In the ‘hero story’ section, CS Ramaswami Kalidas, a veteran in the fraternity critically analyses and shares his views on the role of CS and why the SEBI clarification is a right move in upholding the role. He has beautifully emphasised on the ‘role’ and ‘reporting’ terms. Don’t miss the insightful article !

The architect behind Samhita’s regulatory news updates, CS Rajeswari Pai has analysed RBI’s Digital Lending Directions which can be a good weekend read !

Along with this are the usual ‘culprits’ – many udpates from RBI, MCA, SEBI, ESG, GST, IT, IBBI etc. For any previous issues of Samhita and the readers’ feedback, please visit http://www.sharadasc.com/resource-center/.

Happy Reading

S.C. Sharada

![]() www.linkedin.com

www.linkedin.com

As the fraternity is aware, SEBI has through amendments introduced to the LODR Regulations in the month of December 2024, made a slew of changes to give effect substantially to the recommendations of the Expert Committee appointed by it ostensibly to review the provisions in the above Regulations with the intent to ease considerably the economic environment relating to conduct of business by listed companies in India.

As the fraternity is aware, SEBI has through amendments introduced to the LODR Regulations in the month of December 2024, made a slew of changes to give effect substantially to the recommendations of the Expert Committee appointed by it ostensibly to review the provisions in the above Regulations with the intent to ease considerably the economic environment relating to conduct of business by listed companies in India.

One of the significant changes brought about by way of an amendment relates to the status of the Compliance Officer who is also the Company Secretary of the Company.

Regulation 6(1) of LODR contemplates that a listed company shall appoint a qualified Company Secretary as the Compliance Officer.

A proviso under Regulation 6(1) has been introduced with effect from December 12, 2024, to stipulate that the Compliance Officer shall be an officer of the company in the full-time employment of the company who stands at a level in the corporate hierarchy not more than one level below the Board of Directors who shall also be designated as a “Key Managerial Personnel”. The term “officer” for the purpose of this proviso shall carry the meaning assigned to it under Section 2(59) of the Companies Act, 2013 (hereinafter referred to as “The Act”) and Key Managerial personnel shall be one who is described as such under Section 2(51) of the Act. A Company Secretary falls within the ambit of the definition of the above term under Section 2(51).

Ministry of New and Renewable Energy (MNRE) launched the Green Hydrogen Certification Scheme of India (GHCI) on April 29, 2025 as part of the National Green Hydrogen Mission. The framework of the Scheme provides for certification of green hydrogen production. The certification will not only boost credibility in the market but also the exports of the same. Relevant rules have also been notified for claiming offset under the Carbon Credit Trading Scheme (CCTS).

(Open PIB release dt April 29, 2025)

(Open ESG News dt May 01, 2025)

Recently Microsoft announced launch of new solutions for users of its Azure cloud computing platform, aimed at reducing carbon emissions caused from the cloud’s usage. Sustainability features such as carbon emission analysis, carbon optimization, integration of sustainability factors into daily cloud operations are being introduced.

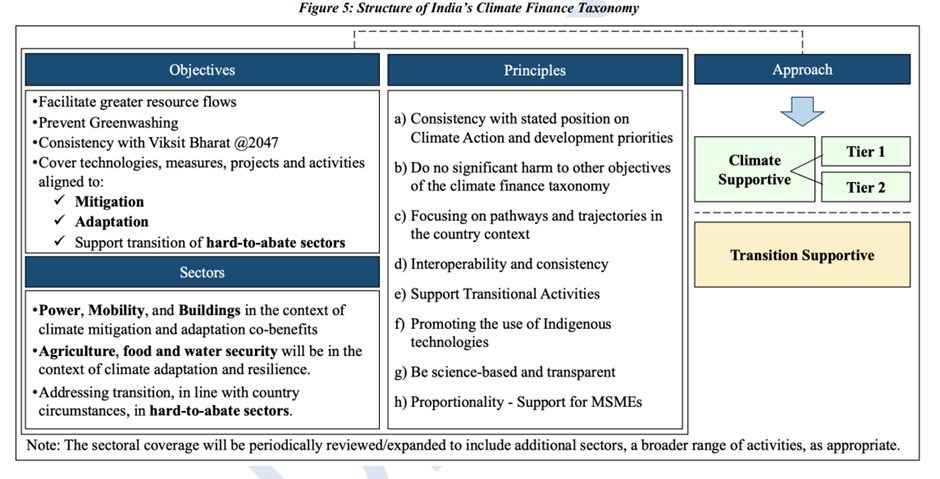

Draft Framework of India’s Climate Finance Taxonomy

In furtherance to Union Budget announcement to develop India’s Climate Finance Taxonomy Department of Economic Affairs, Ministry of Finance has released draft framework for the same. The taxonomy is aimed to facilitate greater resource flow to climate-friendly technologies and activities, enabling India to achieve the vision of being Net Zero by 2070. The Taxonomy covers technology, measures and projects aimed at the following key aspects:

- Mitigation of GHG emissions including through the expansion of non-fossil fuel energy, etc

- Adaptation of resilience action including resilient infrastructure, climate resilient seeds, sustainable water management etc to lower the negative impact of climate change

- Support transition in hard to abate sectors – innovation and R&D that lower carbon pathways by taking into account available technology, its access and viability.

Qualitative aspects aligned with SDGs and quantitative aspects such as GHG savings, improvements in emission intensity etc have been considered for the framework.

The taxonomy aims to prevent Greenwashing and stay aligned with the developmental goal of Viksit Bharat.

Public comments have been invited and the same may be submitted by June 25, 2025