This tiny country falls into one of these categories for most Indians today – bucket list / plans finalized / visited / must revisit. I am firmly in the last category, having recently visited the Land of the Rising Sun—Japan. The place, people, culture, orderliness, discipline, cleanliness, and deep sense of public convenience left me amazed. While Japan has its share of iconic landmarks and scenic beauty, it was the everyday experiences that stayed with me.

When a Nation’s Values Show, all we can say is Arigato gozaimasu (thank you very much) dear Japan !

• Lost and Found

One rainy evening in Osaka, the three of us decided to visit Don Quijote (Donki), the famous maze-like discount store. Though our cab driver took us to the correct location, Google Maps misled us, and we ended up near Osaka Station.

A helpful young woman tried to guide us using Google Translate, but we still couldn’t figure it out. Finally, we did what we instinctively do—stop someone and ask. A gentleman returning from work paused. He didn’t speak English, but that didn’t matter. Instead of giving directions, he simply walked with us—for nearly 1.5 km—through passages and roads, all the way to the store. At the entrance, he bowed, smiled, and quietly left. We just stood there, smiling and bowing back—grateful and slightly overwhelmed. A complete stranger, going out of his way without hesitation. I recalled a similar story shared by a friend, when 20 years ago a stranger in Tokyo accompanied him on the metro to drop him off at his hotel. Such gestures are rare anywhere in the world.

The spirit of Atithi Devo Bhava—a philosophy we proudly claim in India— is being so beautifully practiced elsewhere.

• Was It Really an “Accident”?

On Day 2 of our trip, we noticed our bus driver was missing just as we were about to depart—unusual in a country synonymous with punctuality. Soon, we spotted him near a commercial van, making calls and inspecting something. Within minutes, two police officers arrived on bicycles—equipped with tools and documentation sheets. They carefully recorded details, soon joined by an insurance assessor who measured a barely visible scratch on the van’s rearview mirror.

Yes, that was the “accident”—a minor brush between our bus and the van.

What followed was a masterclass in civility. No raised voices, no arguments, no drama. Every step adhered to the law. Fine paid, the drivers exchanged bows and smiles (not blows and abuses !) before moving on. No bargaining, no threats, no chaos.

After a 45-minute delay, our driver rejoined the bus, bowed deeply in his inimitable Japanese style, and apologized profusely to all of us in Japanese – for something so minor. We were both amused and deeply impressed.

• Age and Mobility

Japan’s aging population is often discussed as a challenge. Yet, what we witnessed was remarkably inspiring. With minimal reliance on domestic help or service personnel, even super seniors remain active, independent, and mobile. They shop, carry their belongings, cross roads safely, and even engage in recreational activities.

While we waited during the “accident episode,” we noticed a cheerful group of elderly men and women—clearly in their 80s or 90s—playing a golf-like game. Slow but steady, they moved gracefully, bending without assistance and playing with enthusiasm that defied age.

We also saw young mothers cycling confidently, managing prams and supplies attached to their bicycles—without nannies or assistance—on safe, well-designed roads.

Clearly, it’s not just infrastructure – it’s a way of life.

• Eliminating the Problem at the Root

What keeps Japan’s cities so impeccably clean? Interestingly, you’ll hardly find trash cans—even in tourist-heavy areas. People carry their waste back home, where it is meticulously segregated into nearly 20 different categories for disposal (as per our Japanese guide).

Yes – 20 bins! The result? Spotless streets, no overflowing garbage, no mess.

In a light-hearted moment at Tokyo’s Meiji Shrine, a local woman told me, “I love your country—so much spirituality.” When I replied, “I love yours—it’s so clean,” she laughed and said, “No, no… it is too clean!”

We’ve all seen Japanese spectators cleaning stadiums after sporting events. This behaviour is deeply ingrained in their culture.

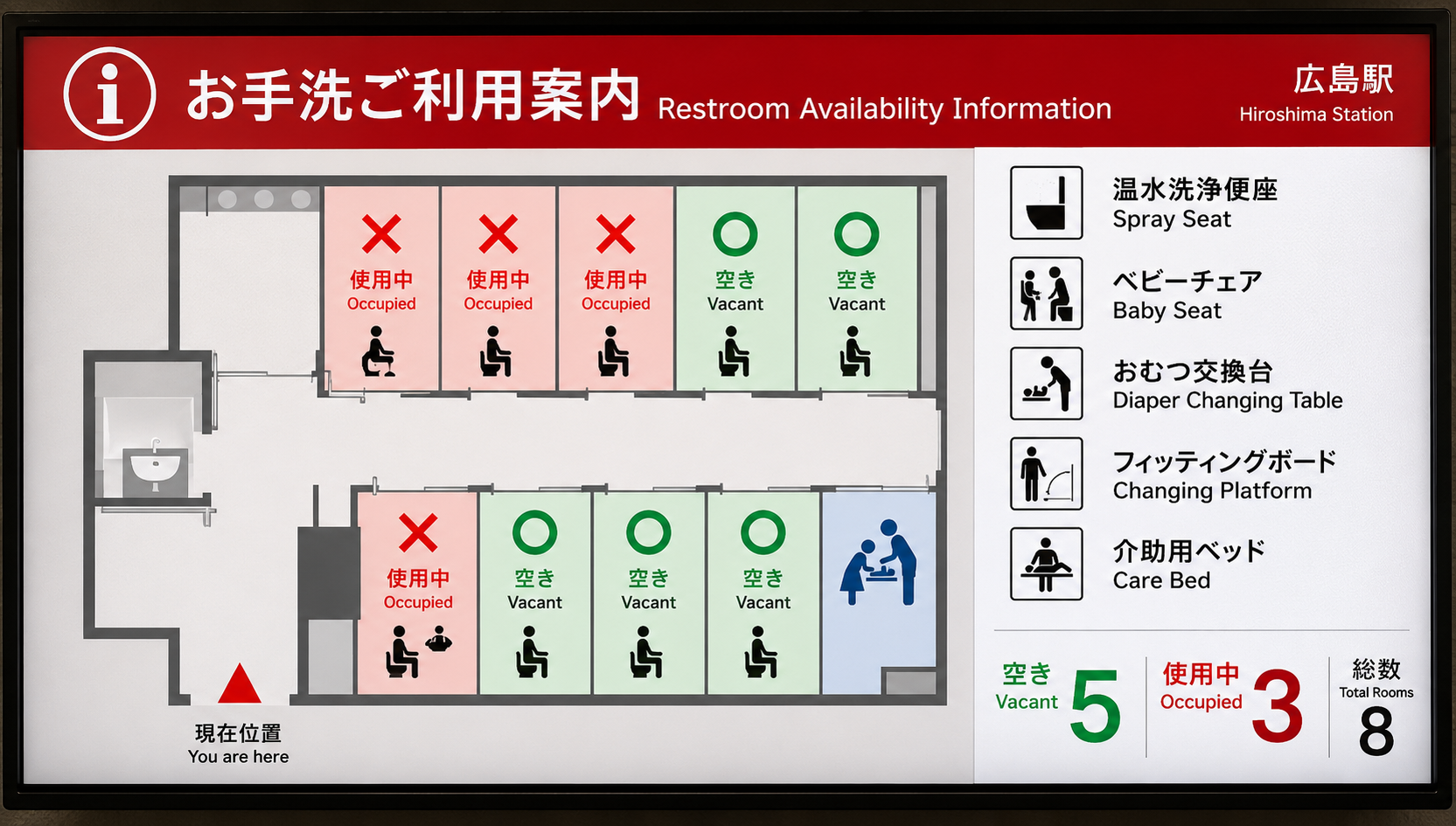

• Clarity and Public Convenience

Japan’s commitment to public convenience is evident everywhere.

From the abundance of clean, well-maintained toilets to clearly marked instructions—everything is thoughtfully designed. Of course, the high-tech toilets, with their array of buttons and symbols, created moments of both confusion and amusement!

Queue systems are strictly followed, with even a dashboard showing vacant-occupied toilets! Be it metro stations, Shinkansen trains, shrines, or public spaces—clear instructions and organized systems reflect a deep respect for people’s time and comfort.

• A Thought to Take Back

If a small country can demonstrate such discipline, cleanliness, and civic sense, why not us?

The answer perhaps lies in mindset—shaped early in childhood. I am told, in Japan, children up to the age of 5 or 6 are taught values of cleanliness, responsibility, and discipline before academic rigor.

That foundation shows.

As for me, I would dearly love to return—this time at a slower pace, to absorb even more of its beauty, culture, and way of life.

Arigato gozaimasu dear Japan for your hospitality and lessons !

Back home, we switch gears to a different kind of complexity—regulatory changes. The 325th issue of Samhita brings together key updates from multiple regulators with the aim of making them easier to navigate.

For previous issues and to share your feedback: 👉 http://www.sharadasc.com/resource-center/

Happy Reading

S.C. Sharada

![]() www.linkedin.com

www.linkedin.com

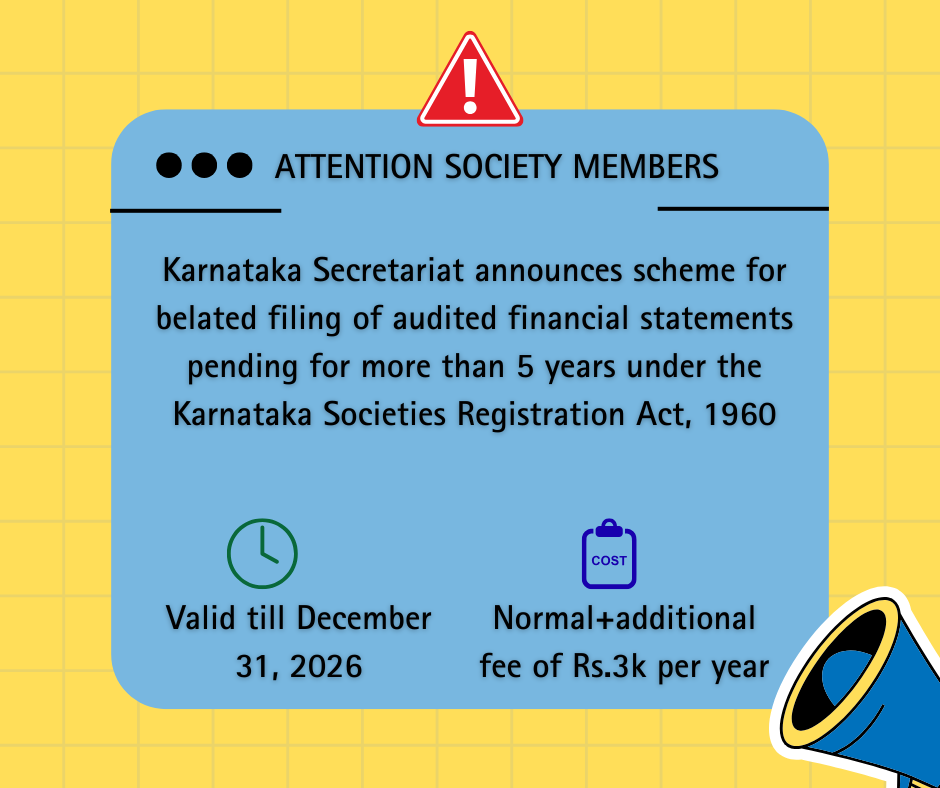

Scheme announced for filing pending annual returns under the Karnataka Societies Registration Act, 1960

Scheme announced for filing pending annual returns under the Karnataka Societies Registration Act, 1960

A society registered under the Karnataka Societies Registration Act, 1960 is required to file its audited financial statements every year with the Registrar of Societies (RoS), within 15 days of holding its Annual General Meeting. This is required for the yearly renewal of the registration. The Karnataka Government Secretariat vide circular dated May 27, 2026 has announced a scheme under which Societies which have not filed their audited financial statements with the ROS for more than 5 years have been allowed to file the same with an additional fine of Rs. 3,000/- per year. The opportunity to file belated returns is valid till December 31, 2026.

Unlike other regulators, these circulars are difficult to trace online and through this newsletter we bring this to the attention of relevant stakeholders. It is pertinent to note that while the provisions under the Income Tax Act, 1961 may not require the financial statements of a Society to be audited if it does not breach certain threshold, the Karnataka Societies Registration Act, 1960 requires the same and the RoS strictly insists on this aspect.

Considering multiple societies function with limited awareness of the requirement to file audited financial statements with the Registrar, it may be useful for the relevant stakeholders to avail this scheme for renewing their registrations. Further, this is useful for those societies who are planning to register/list on the Social Stock Exchanges (SSE). Timely renewal can open ways for registration on the SSE.

(Open original Notification dt May 27, 2026)

(Open Translated version of the Notification)